Over the past few years, Southeast Asia has become one of the most active regions for Chinese companies expanding overseas. According to the e-Conomy SEA Report published by Google, Temasek, and Bain & Company, Southeast Asia’s digital economy is expected to reach USD 600 billion by 2030, and in certain scenarios could approach USD 1 trillion. A young population structure, widespread mobile internet adoption, and a rapidly growing e-commerce ecosystem continue to attract cross-border merchants to the region.

However, as more companies expand from selling in a single country to operating across multiple Southeast Asian markets, new challenges are gradually emerging. Many merchants entering their second Southeast Asian market discover that the same products and marketing strategies can produce very different conversion results across countries. Payment processes that worked smoothly in one market may also encounter adaptation challenges in another.

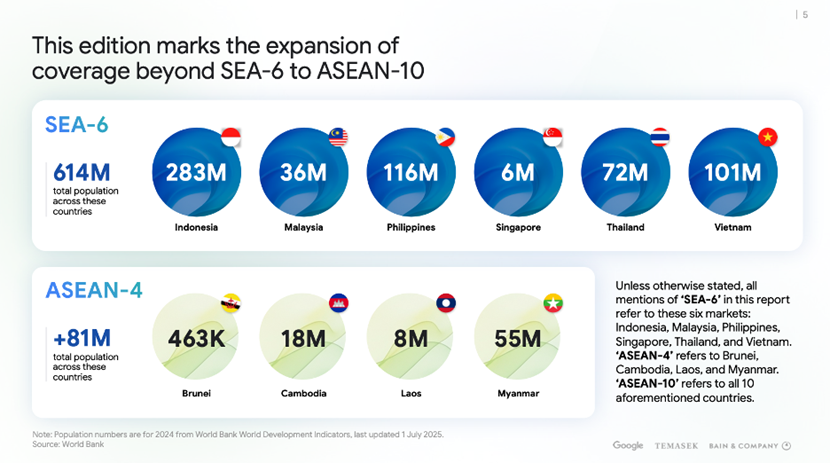

Source: e-Conomy SEA Report

What this reflects is not an issue within a single market, but a fundamental characteristic of Southeast Asia’s business environment: Southeast Asia is not a single market, but a region composed of multiple national markets. As business expands from one country to several, the complexity of operations increases significantly.

Southeast Asia Is Not One Market, but Multiple National Markets

In the early stages of cross-border e-commerce expansion, many companies approach Southeast Asia as a single “regional market.” However, as operations deepen, businesses quickly realize that countries across Southeast Asia differ significantly in consumer behavior, payment ecosystems, and regulatory environments. For example:

- Indonesia: High adoption of e-wallets and rapidly growing digital payment penetration.

- Thailand: A well-established real-time bank transfer ecosystem.

- Malaysia: A mix of card payments and local payment methods.

- Vietnam: Rapid growth of e-wallet adoption, while cash on delivery (COD) remains present in some scenarios.

At the same time, several Southeast Asian countries are actively building national payment infrastructures. Systems such as Indonesia’s QRIS, Thailand’s PromptPay, Singapore’s PayNow, and Malaysia’s DuitNow are gradually becoming key components of local digital commerce and are shaping consumer payment behavior.

As a result, when businesses expand from one country to multiple markets, they often need to adapt to different payment ecosystems, rather than simply replicating an existing operational model.

Payment Differences Are Often the First Change Businesses Notice

In a multi-country operating environment, payments are often the first area where businesses experience noticeable differences. The reason is straightforward: payments sit at the intersection of consumer habits and local financial infrastructure. When entering a new market, if payment methods do not match local consumer preferences, transaction conversion can be directly affected.

- In markets where e-wallets are widely used, offering only card payments may significantly reduce transaction completion rates.

- In countries where real-time bank transfers are common, complex payment flows may increase the likelihood of payment abandonment.

In this context, as businesses expand from a single country to multiple markets, local adaptation of payment methods often becomes the first operational hurdle companies must address.

The Complexity of Multi-Country Operations Goes Beyond Payments

As companies expand into more Southeast Asian markets, the challenge often shifts from how to complete a transaction to how to maintain stable transactions, manage funds, and control risk across multiple markets. In practice, this typically involves several key areas:

1. Local payment method coverage

Consumer payment preferences vary significantly by country. E-wallets, real-time bank transfers, card payments, and in some markets cash on delivery (COD) mean that businesses must maintain flexible payment integration capabilities.

2. Multi-currency fund management

Regional operations require companies to handle multiple local currencies simultaneously—such as the Indonesian rupiah, Thai baht, and Vietnamese dong—and manage settlement and fund allocation across different markets.

3. Regulatory and compliance environments

Financial regulatory frameworks across Southeast Asia are not unified. Companies operating in different markets must pay close attention to local payment regulations, data compliance requirements, and rules governing fund flows.

When these factors combine, businesses are no longer dealing with the operational challenges of a single market, but with the structural complexity of multi-country operations.

As Business Expands, Transaction Stability Becomes a Core Capability

In multi-country operations, businesses need to focus not only on order growth but also on whether their transaction infrastructure can remain stable across different markets. This means ensuring that:

- Payment methods align with local consumer preferences

- Transaction flows maintain a stable user experience across countries

- Settlement processes support multi-currency management

- Risk management and compliance requirements are effectively addressed

Only after these foundational capabilities are established can companies achieve stable development across multiple markets.

Southeast Asia Expansion Is Entering a New Phase

Southeast Asia remains one of the most dynamic regions for global digital commerce. However, as the market matures, the operating environment is also evolving. In the early stage of expansion, the key challenge for companies was how to enter a single market. As businesses expand further, the question increasingly becomes how to operate sustainably across multiple national markets. This challenge involves not only product and marketing strategies but also foundational capabilities such as payments, fund management, and regulatory compliance.

As multi-country operations become the norm, payment systems are evolving from simple transaction tools into core infrastructure supporting regional business operations. Oceanpayment has long supported global merchants and continues to accumulate experience in multi-market payment integration, local payment method coverage, and cross-border fund settlement, helping merchants complete transactions and manage funds more reliably across complex regional environments.

For companies expanding into Southeast Asia, entering the region is no longer simply about accessing a new market. It is about building the ability to operate across multiple national markets over the long term. Only when businesses can maintain stable transaction and fund flows across different countries can Southeast Asia’s growth potential translate into sustained business expansion.

References

- Google, Temasek & Bain & Company — e-Conomy SEA Report

- FIS — Global Payments Report

- Bank Indonesia — QRIS Official Information

- ASEAN Secretariat — Regional Payment Connectivity Initiatives

粤公网安备 44030502003453号

粤公网安备 44030502003453号

Comments are closed.